Periodic vs. Perpetual Inventory System – Definitions, Benefits, Examples

Although a periodic inventory system might seem clear-cut and foolproof at first glance, its disadvantages may outweigh the benefits. Perpetual inventory systems, however, are already becoming mainstream.

What is a Periodic Inventory System?

A periodic inventory system is a bookkeeping method based on counting and marking down your items. It means updating the inventory balance periodically, at the beginning and at the end of an accounting period. This also means that the books are only accurate periodically.

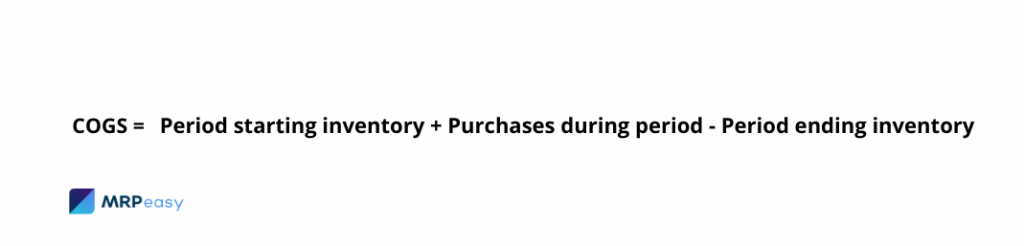

To update the inventory balance, stock take (i.e. a physical count) is used to measure the level of inventory and to calculate the cost of goods sold (COGS).

Because manufacturing companies often carry inventory items in the thousands, stocktake could be very time-consuming. That is why a physical count is usually performed once a month, once per quarter, or even less frequently.

Accordingly, the inventory account and cost of goods sold (COGS) numbers are current only once per period – in the time directly after stocktake.

Furthermore, in a periodic inventory system, purchases are recorded in a separate purchases account from where information passes on to the inventory balance only at the end of the accounting period.

A periodic inventory system does not rely on software that would allow for real-time inventory tracking. Therefore, it would be feasible to use periodic inventory if dealing with low volumes of products or materials.

Good examples where a periodic inventory would be suitable are motor vehicle dealerships, art galleries, haute couture makers, and other low-volume producers and sellers.

For most manufacturers, however, keeping a periodic inventory system could prove to be insufficient.

Periodic inventory accounting

The accounting principles of periodic inventory are quite simple and straightforward, with not many transactions regarding inventory.

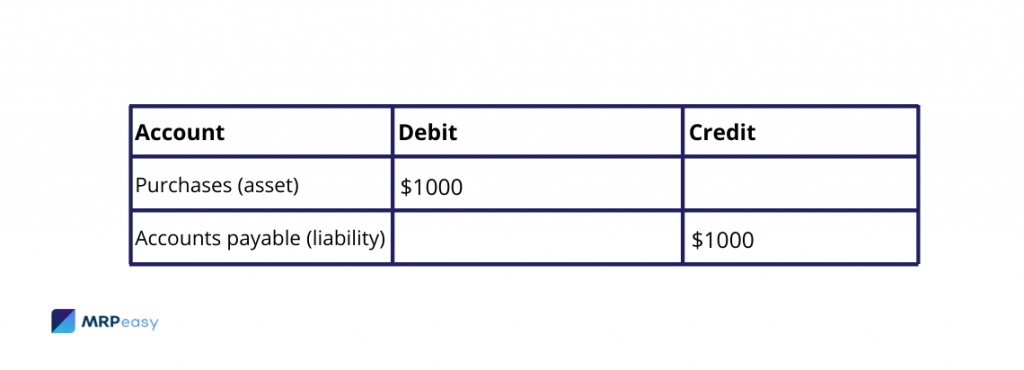

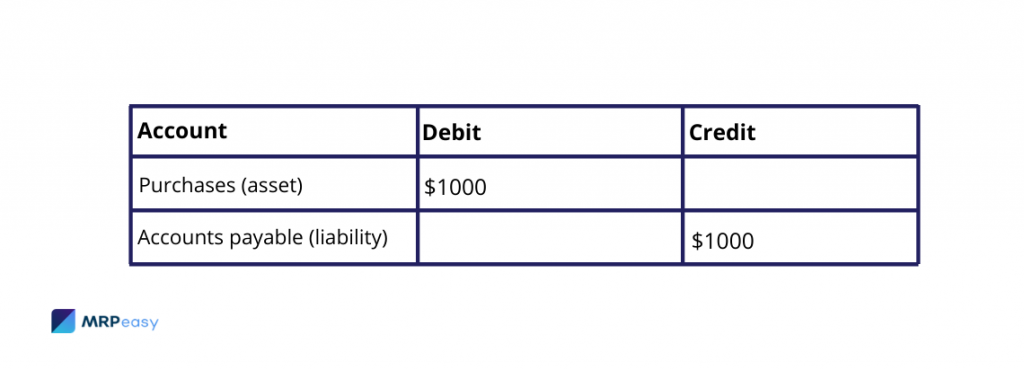

When goods are purchased, they are accounted for in a purchases account, which shows the sum of all purchases during the period.

At the end of the accounting period, the sum of purchases during the period is carried to the inventory account.

Let’s say that at the beginning of the period, the inventory balance was $500.

The inventory account now holds the sum of beginning inventory plus purchases: $500 + $1000 = $1500.

An inventory count is carried out, which provides the actual ending inventory balance of $250.

According to the COGS formula, we find that the COGS in the period is $1500 – $250 = $1250.

This amount is taken from the inventory account, and expensed.

Now, our accounts are up to date: we have $250 of stock, and the COGS in the period was $1250.

If we sold our products for a total of $2000, the profit would be $2000 – $1250 = $750.

What is a Perpetual Inventory System?

Perpetual inventory, also known as continuous inventory, is a software-aided inventory system that is updated automatically and continuously, as opposed to manually and periodically. All movements in stock, both inward or outward (i.e. purchases, returns, consumptions, and write-offs) are always accounted for. This means that the books are up to date at all times.

Most modern cloud-based inventory management systems are perpetual, using barcodes, POS systems, radio frequency identification, and real-time reporting to track changes.

A good example of a perpetual inventory system would be an MRP software which acts as infrastructure between different departments of a manufacturing business, making the exchange of information instantaneous.

All actions pertaining to the manufacture – sales, purchases, inventory movements, shop floor activity, etc. – are recorded in the software, and shared with the relevant parties. This way, all departments have the information they need at hand at all times.

The bottom line is this:

A perpetual approach gives a more detailed and current oversight of both stock and COGS, allowing companies to make business decisions based on up-to-date information and stock levels.

Although a perpetual inventory system automates a lot of processes related to stock and accounting, it is still necessary to perform occasional stocktakes (like once a year) in order to account for unrecorded movements, errors, theft, or other discrepancies commonly referred to as phantom inventory.

Read more about How Stocktake Helps Prevent and Detect Theft

Perpetual inventory accounting

In manufacturing, there are constant changes in inventory.

With a perpetual inventory system, you can track and record the changes immediately in order to keep the books accurate.

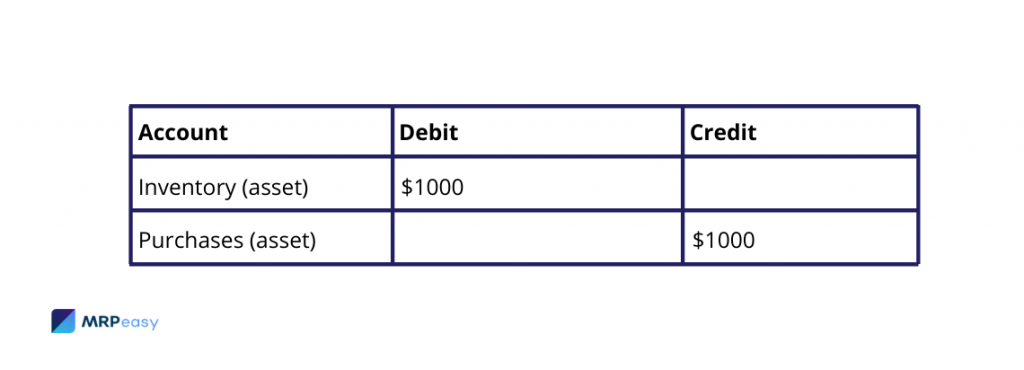

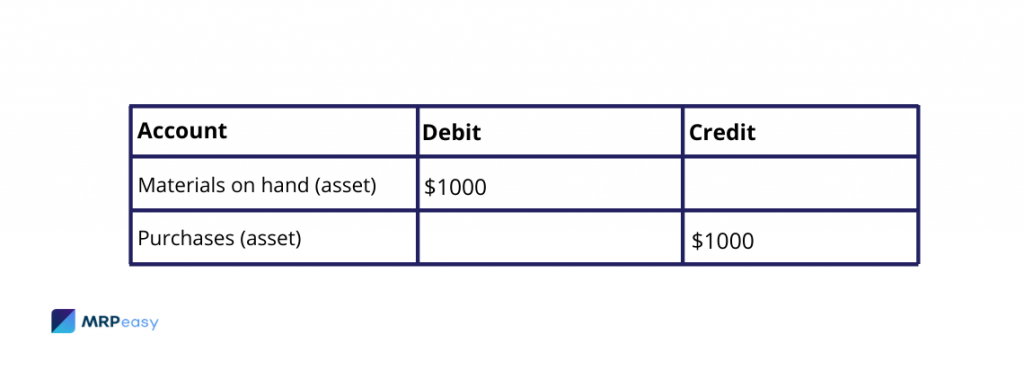

When a purchase is placed to a vendor and you receive the invoice, it is recorded in an asset account, showing the sum of purchased goods which have not yet been received (goods that your vendors owe you).

Once the purchased goods are received, their value is transferred from the purchases account to a corresponding inventory account.

E.g. if a manufacturer purchases materials, the account for these could be “Materials on Hand”.

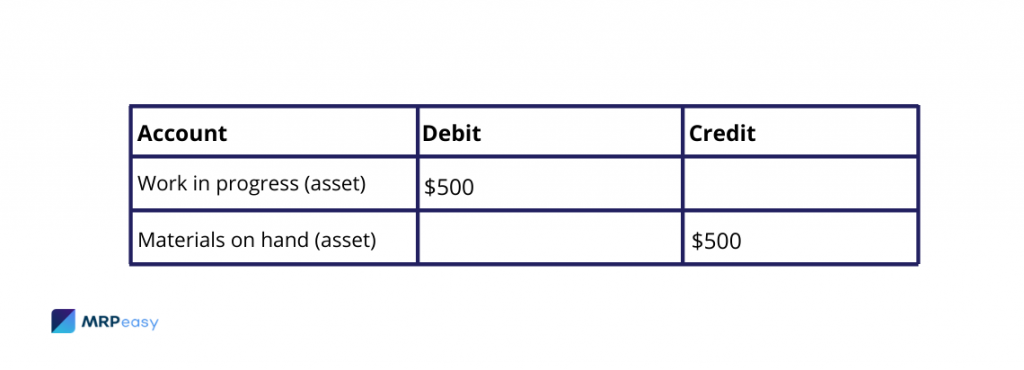

When some materials are used in manufacturing, their cost is carried to a Work in Progress (WIP) account, which shows the current (not final) value of the products which are being manufactured at that moment.

E.g. if half of the materials procured in the previous step are used:

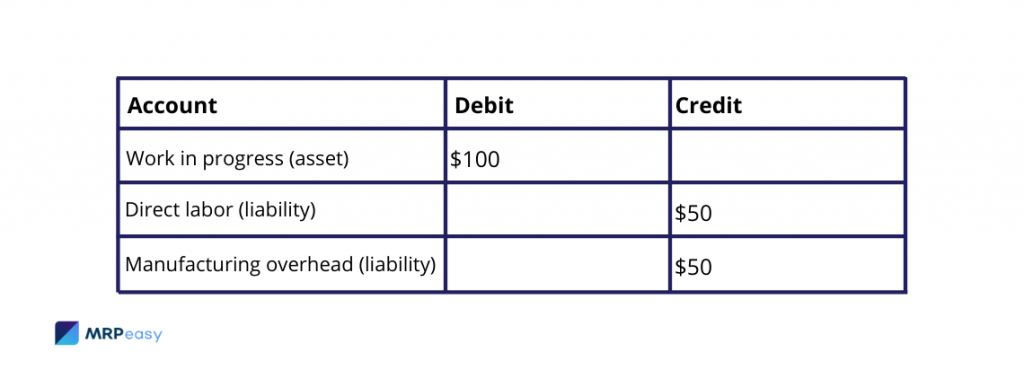

Additionally, it is possible to include the cost of direct labor and manufacturing overhead (aka factory burden) in the cost of the finished goods via the WIP account.

In such a case, this portion of payroll and factory expenses is not going to show up in expenses immediately, but only when products are sold.

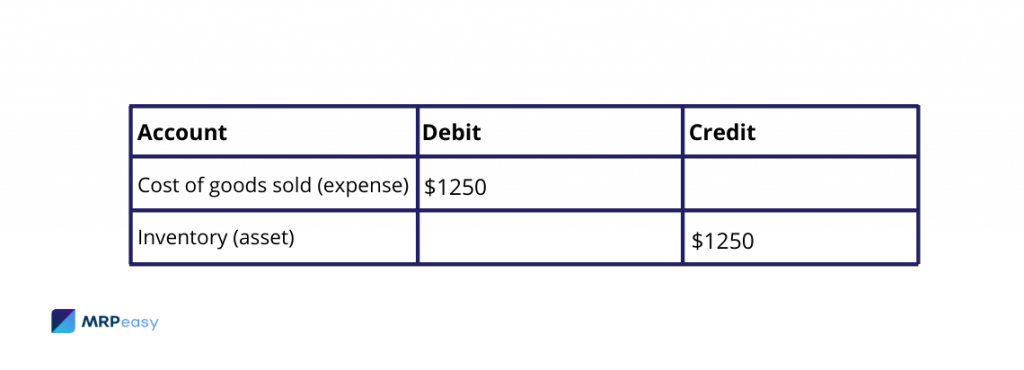

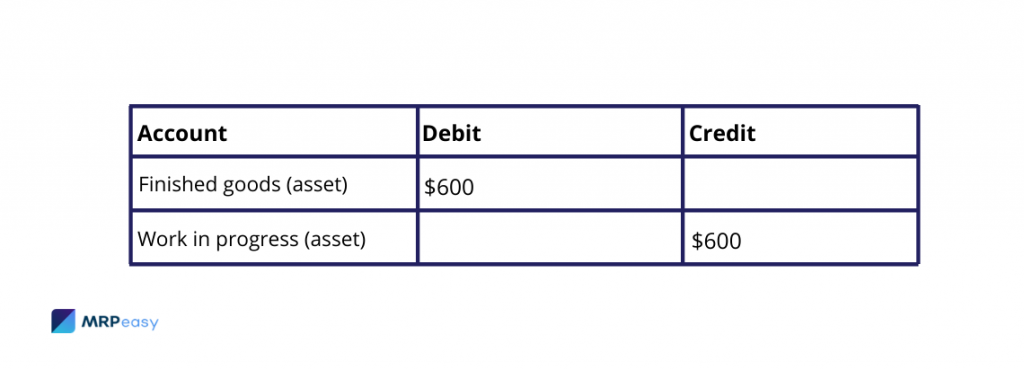

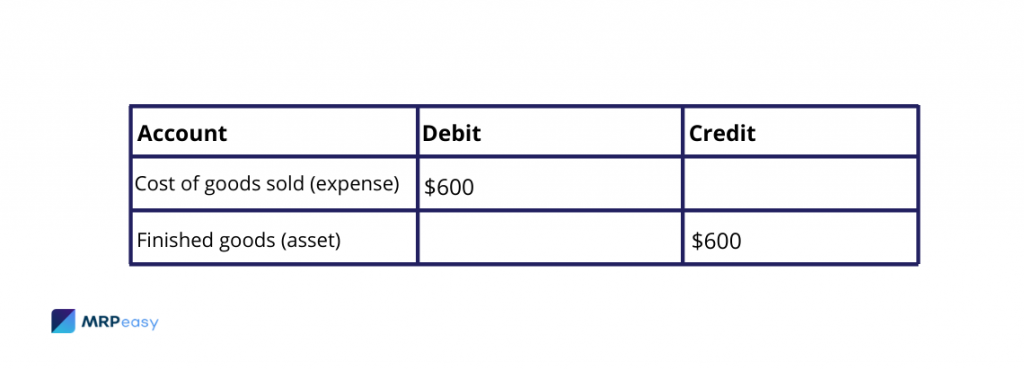

When manufacturing is finished, the final cost of the finished products is moved from the work in progress account to a finished goods inventory account.

Once products are shipped to the customer, these are carried to expenses:

When we subtract COGS from what our customer paid us, e.g. $1000, we immediately find that the profit is $1000 – $600 = $400 for this sale.

Thus, we have highly specific information in real-time and we do not need to wait for an end of the period stocktake to make our next decisions.

Pros and cons of periodic inventory systems

As periodic inventory is as old as history itself, it is also quite primitive. Even though it is a reasonable choice for companies just starting out, it has some disadvantages that could become issues in the long run.

Pros:

- Easy to implement

- Sufficient for companies with low volumes

Cons:

- Ultimately complex due to manual entries and calculations

- Prone to human error

- Up-to-date only periodically, immediately after a stocktake

- The bigger the inventory, the bigger the risk of discrepancies

- Vulnerable to stockouts

- Business shut-downs during stocktake

- Theft is more difficult to notice

Pros and cons of perpetual inventory systems

Perpetual inventory systems bring a lot of advantages to the table, yet there are still some things you need to look out for.

Pros:

- More accurate

- Always up-to-date

- Suitable for inventories of all sizes

- Work in progress accounting

- Real-time cost of goods sold and profit/loss overview

- More data to guide informed business decisions

- Lower risk of stockouts or overstocking

- Less time wasted on stocktake and accounting

- Reduced risk of human errors during stocktake

- Less chance of theft

Cons:

- The accounting principles are more complicated

- Events must be reported in real-time and correctly to get correct results

- Extra costs for software

- Takes more time to properly implement

- Still needs an occasional stocktake

Myth: Perpetual inventory systems are expensive and difficult to implement

Truth: Perpetual inventory systems used to be expensive and difficult to implement

It is a common misconception that perpetual inventory systems cost a lot and take months, if not years, to implement. In reality, this belief is a relic from days gone by. Because with the advent of cloud computing and manufacturing SaaS providers, this changed radically. Modern manufacturing software with integrated inventory management modules is affordable even to the smaller players. And even though implementing one does require a united effort, it is nowhere near as time and resource-consuming as it was ten years ago.

True, software still costs money. But you know what costs more? The labor you use in order to perform stocktakes and accounting tasks. The business lost due to stockouts. The discrepancies that add up over time. And the bad decisions caused by gaps in inventory accounting.

Conclusion

Perpetual inventory systems come out as the clear winners in the fight with their periodic counterparts in a huge majority of cases.

Practically, if you run a manufacturing business, you will do better by implementing a perpetual system early on.

Unless you have very few inventory transactions and do not even plan to expand. And that is probably not the case.

While using perpetual inventory, you should still add periodic elements like periodic stocktakes to your inventory accounting. Periodic stocktakes will help you detect any discrepancies that have slipped in and which the perpetual system has not accounted for.

By combining the two approaches, your inventory accounting should be in tip-top shape.

You may also like: Inventory Control – What is it and Why is it Important?