What Is Job Costing and How to Do It?

Job costing means tracking the costs related to individual orders. This allows accounting to measure the profitability of each project separately and to use it as a basis for customer quotes and financial planning.

You can also listen to this article:

What is Job Costing?

Job costing is a systemized way of tracking and monitoring production expenses, with each “job” representing an order from a customer. In this way, companies can produce larger or smaller quantities of finished goods while keeping production within predictable costs.

In manufacturing companies, few things are as important as cost. If production costs are correct, the company can comfortably measure profitability to hit targets for margin. They can also benchmark themselves with competitors to understand what they need to improve. And they can plan budgets and operating expenses confidently over long periods.

Generally, there are three areas that most manufacturers track: labor, material, and overhead. Calculating these costs within manufacturing is often done using job costing.

Basic Job Costing

Basic job costing consists of the cumulative sum of labor, material, and overhead for each job. Here are some considerations for each:

Labor

Labor is the cost required to employ team members and staff needed for production. Many costing systems refer to this as direct labor, or the labor needed to perform the production tasks required to produce the units in each order. It does not include administrative, which is calculated differently and included in the overhead component.

Labor may also include any subcontractors or temporary labor used in the completion of orders. This can become more complicated when elements of assembly are done by the subcontractor offsite. However, they must be included to be accurate.

Companies must make sure to include the total cost of direct labor. This means that not only the hourly rate of the employee must be considered. It must include a net upward of costs incurred by the company for benefits, training, government compliance such as unemployment, and many other factors. In some locations, this net upward can be as high as 30-40% on top of the base hourly rate, and miscalculation will throw off the job cost.

Other considerations include whether the size of the order will trigger overtime. It may also be impacted by staff training, where unskilled temporary workers or subcontractors may not perform at the regular rate compared to regular company employees.

Material

Material encompasses all raw materials and components used in the production of finished goods. It includes things such as nuts, bolts, housings, motors, etc. But it must also include consumables. Consumables may take the form of gloves or masks that can only be used once during production as well as testing supplies, “lead-in” and “trail-off” material for the start and stop of the run, and even the weld material, glue, and other fasteners that may melt or disappear during production. Delivery cost may also be included as an actual cost or an average cost added to the overall material line.

Material would seem to be a straightforward calculation. And in some industries, it is. For example, in a manufacturing company that produces metal clothes hangers, material can be precisely measured per unit. However, in batch operations where blending or mixing require precise formulas or in operations where material is lost through evaporation or absorption, a calculation may be more difficult.

Order size may also impact material cost. Many vendors have a minimum order quantity or offer tiered pricing on raw materials and components to capture economies of scale for their own operation. Using the above example of the coat hanger manufacturer, an order of 1,000 units where the manufacturer must order the wire separately will cost more per unit than an order of 100,000 units if the vendor offers volume-tiered pricing. So, order size must factor in based on knowing these minimums or tiers.

Overhead

Overhead is often the most difficult to calculate accurately. Much of this has to do with the type of manufacturing done. At its most basic, overhead will include rent, property tax, administrative costs, equipment depreciation, and other factors. If the enterprise has an extensive design or engineering staff for example, then the overhead will be higher than a company that outsources design talent or has no need.

Another difference in the overhead application is that it is a direct proportion compared to labor and material. Labor and material are costed using actual costs, but administrative, rent, engineering, and other tasks are utilized to produce all finished goods. This makes it difficult to estimate.

For example, while 100,000 units of clothes hangers may require three labor technicians and $1000.00 of material, the administrative assistant is a single salary in a company producing the hangers and a dozen other products. The same applies to other cost centers such as rent. How to calculate overhead is therefore tricky.

Many companies may use a “standard” overhead cost for all products that have been calculated and honed over time. The risk of setting this average too high means that the company may set prices too high as well, hurting competitiveness. Or it may set the overhead average too low and erode margin over time.

In fact, for being able to accurately estimate overhead per job upfront, there must be a good production plan or capacity plan for the future period. Then, it is possible to sum up all the predicted overhead costs and either:

- calculate an hourly overhead rate, by dividing these costs with the estimated labor or machine hours, which can then be applied to each job according to its duration, or;

- calculate a piece rate, by dividing these costs with the estimated total output, which then can then be applied to each job according to its quantity.

Read also about Applied Overhead vs. Actual Overhead.

When to use Job Costing

Although application and accuracy may vary depending on production mode, many manufacturing companies are ideally suited for job costing. The more standardized and predictable manufacturing processes are, the more accurate the costing. In all cases, this tracking system uses a customer order as a trigger. These orders may come in the form of batches, specifications, or volumetric mass requirements.

- Make to Stock (MTS) – In MTS, manufacturing processes are often highly automated and produce in large quantities. This allows for lower labor costs and accurate measurement of quantities of material used. Costing in MTS is often highly accurate, with material and labor accurately measured in fractions of a cent. The same is true of overhead as overhead costs are spread out over thousands or even millions of units.

- Make to Order (MTO) – MTO manufacturing is often used for big-ticket, high-cost goods and can be costed using the same three methods. Material cost is often the most accurate component of MTO, but close attention to labor may be required to control labor cost. Customization of MTO products may negatively influence overhead as well.

- Assemble to Order (ATO) – Common in the electronics industry, ATO allows accurate costing of all three elements with some attention. Training must be on pace, or else both labor and material may waste and increase the cost. Overhead may be more variable depending on what is ordered and the velocity of the production for each part.

Generally, costing is more complex in companies with many different product iterations and those where services may be included as part of the production.

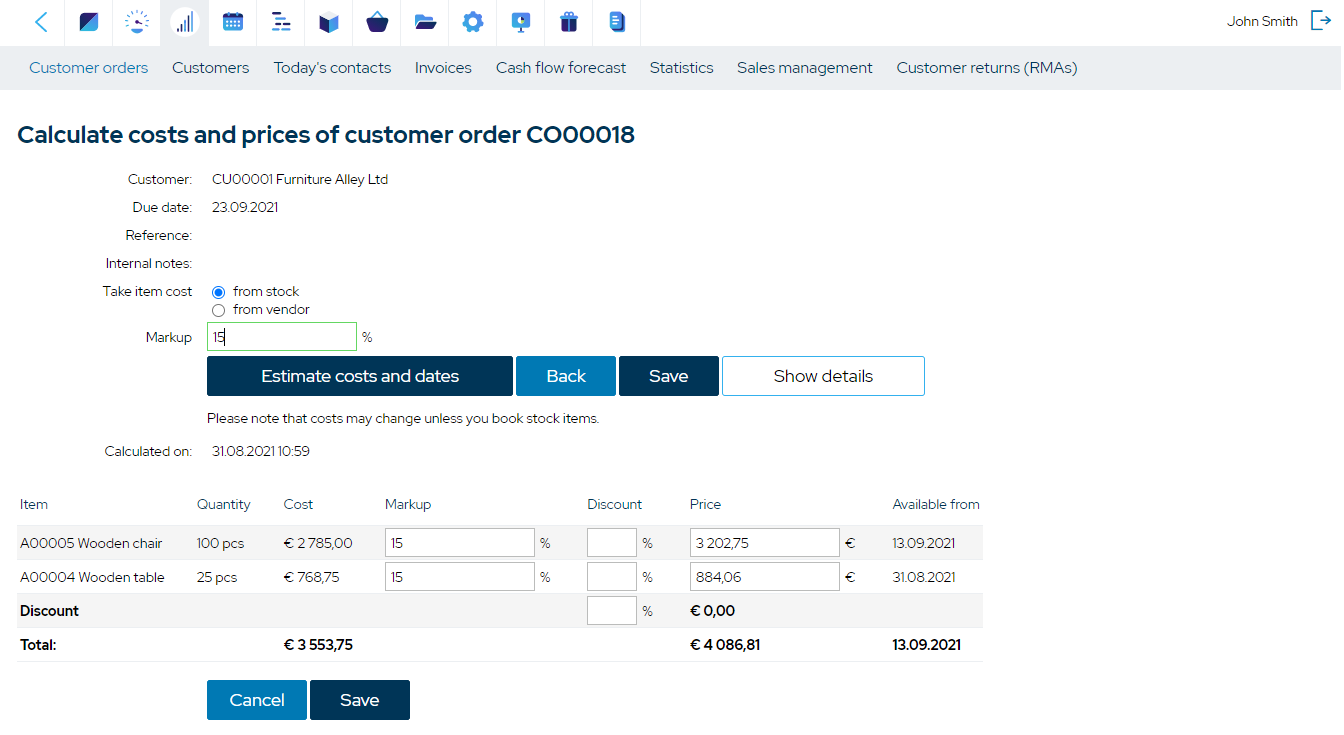

Using software for accurate Job Costing

Size, volume, mode of production, the complexity of the enterprise, and product complexity all make costing a challenging endeavor for any product. When this is multiplied by many products within a single company’s product line, it can become too much to be done accurately.

The traditional way to address this was through close manual calculations, constant reassessment, spreadsheets, and calculators. But in modern manufacturing, this can quickly become overwhelming.

Today, advanced, cloud-based manufacturing software can help manage cost calculations to improve accuracy regardless of the mode of production. This software usually includes detailed multi-level BOMs that can be broken down to the cost level of each item across multiple levels.

These bills of materials can be tied to labor centers for each order as well as real-time inventory. It will also provide accurate automatic planning at a costed level and help drive realistic production schedules to optimize the cost of production.

Because automated manufacturing software links labor, material, and overhead functions, costing can be improved significantly. Routings, BOMs, capacity planning at the workstation level, material planning and reporting, workforce planning, parameter-driven BOMS, and many other features combine to provide manufacturing cost tracking to optimize production and help companies manage an extensive product line with accurate costing.

Key takeaways

- Job costing is a systemized way of tracking and monitoring production expenses, with each “job” representing an order from a customer.

- Correct production costs help the company measure profitability, benchmark itself with competitors, and plan budgets and operating expenses confidently over long periods.

- Basic job costing consists of the sum of direct labor, material, and overhead for each job.

- Direct labor is the cost required to employ team members and staff needed for handling production tasks. Indirect labor such as administrative staff salaries are part of the manufacturing overhead.

- Material encompasses all raw materials and components used in the production of finished goods, including indirect materials like nuts, bolts, adhesives, etc.

- Overhead includes rent, property tax, administrative costs, equipment depreciation, and other factors. As overhead is used in the production of all goods, it is often difficult to estimate, especially when there is no concrete production or capacity plan for the period.

- Job costing gets more accurate the more standardized and predictable the manufacturing processes are. It is a good option in MTS, MTO, and ATO environments, but could become very complex when a company makes products with many different iterations and when services are included as part of production.

- Traditionally, job costing has been done using manual calculations and frequent re-assessments. This, however, can quickly become overwhelming.

- Using an ERP/MRP system can help companies do job costing quickly and efficiently.

You may also like: How to Calculate the Selling Price of Your Products?